Opendoor is the largest iBuyer in the US - a tech

company that buys homes directly from sellers for cash (close in 14 days) and resells

them. Think "CarMax for homes."

The transformation: New CEO Kaz Nejatian

(ex-Shopify COO, $1 salary) is "refounding" Opendoor as an AI-first software company.

Doubled acquisition speed in 7 weeks. Targeting profitability by end of 2026.

The opportunity: $2T residential real estate

market, ~1% iBuyer penetration. If Opendoor captures 3-5% with sustainable margins, it's

a $50B+ company.

A new dawn for real estate: Opendoor's mission to

simplify home selling

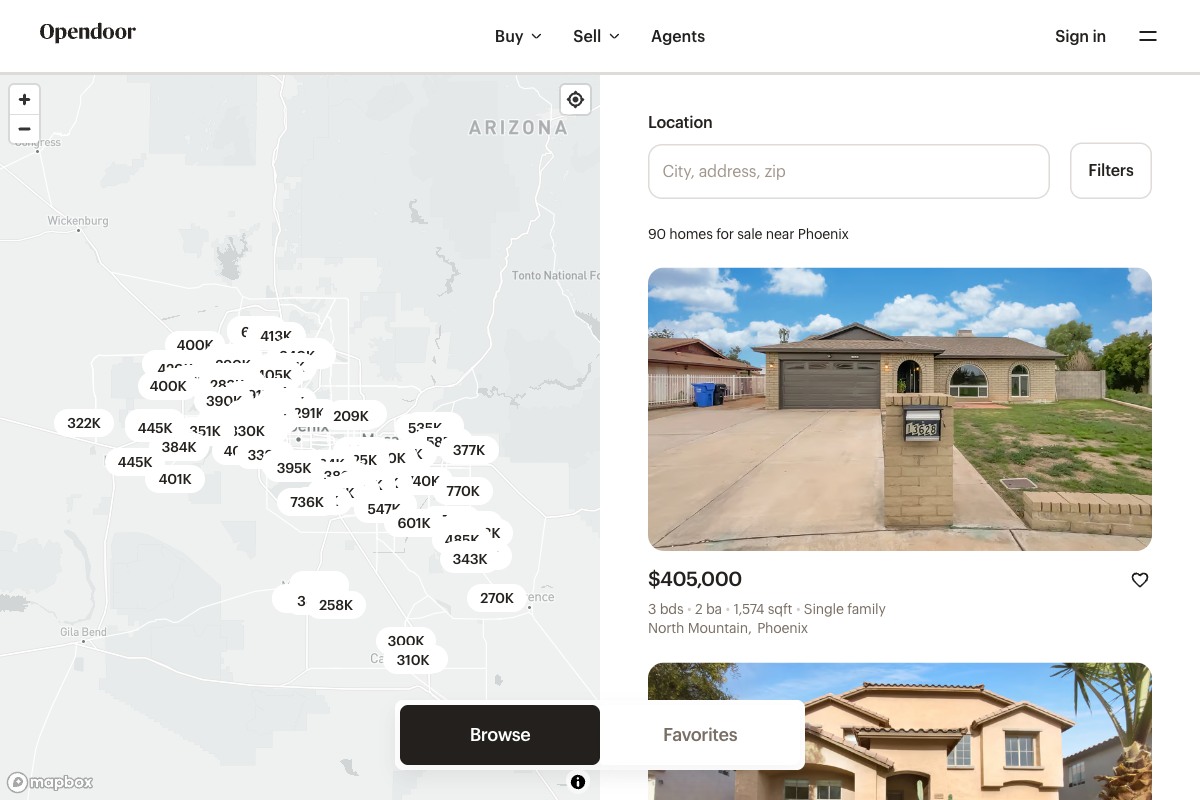

What is Opendoor?

Opendoor is the

largest "iBuyer" in the United States - a technology company that buys

homes directly from sellers with a cash offer, then resells them on the open market.

Think of it as "CarMax for homes." Instead

of listing your home, hosting showings, negotiating with buyers, and waiting months for

a sale - you can get a cash offer in 24 hours and close in as few as 14 days.

The trade-off: You typically get ~5-7% less

than market value. But for many sellers, the certainty, speed, and convenience are worth

the cost.

Why Does Opendoor Exist?

Selling a home is one of the most stressful, time-consuming transactions most people ever

experience:

The Traditional Process

3-4 months average time to sell

Dozens of showings with strangers

Repairs, staging, open houses

Uncertainty until closing day

Coordinating with agent, buyer, lender

The Opendoor Process

Cash offer in 24 hours

Zero showings required

Opendoor handles all repairs

Guaranteed closing date you choose

One company handles everything

Who Should Know About Opendoor?

This guide is essential for:

New employees joining Opendoor who need to understand the business

Investors evaluating OPEN stock and the iBuyer market

Real estate professionals understanding the competitive landscape

Tech industry observers following the Kaz Nejatian AI transformation

Anyone curious about how technology is reshaping real estate

Key Terms Glossary

iBuyer — "Instant Buyer." Company that uses technology to make

instant cash offers on homes.

Contribution Margin — Revenue minus direct costs per home.

Opendoor targets 5%+ for sustainability.

Spread — Difference between buy price and sell price. Opendoor's

profit after costs.

Service Fee — Opendoor's fee to sellers (typically 5%). Covers

pricing risk and convenience.

Eric Wu founded Opendoor in 2014 after experiencing the pain of selling his own home. His

insight: the traditional home selling process hadn't been meaningfully improved in decades,

despite technology transforming nearly every other major transaction in our lives.

"The median homeowner spends 3-4 months selling their home. What if we

could make it as simple as selling your car to CarMax?"

Eric Wu, Founder & Former CEO

Key Milestones

2014

Founded in San Francisco. First market: Phoenix, AZ -

chosen for its large, homogeneous housing stock and predictable appreciation

patterns.

2015

Y Combinator (W15). Raised $9.95M seed round from Khosla

Ventures. Purchased first 35 homes.

2016-2018

Rapid expansion to 18 markets. Raised $325M Series D at

$2B valuation. SoftBank Vision Fund invests $400M.

2020

Goes public via SPAC merger with Social Capital Hedosophia

II. Valued at $4.8B. COVID briefly pauses operations.

Interest rates spike. Q3 losses of ~$1B. December: Eric Wu

steps down as CEO, CFO Carrie Wheeler takes over. 18% layoffs.

2023

Continued inventory challenges. Additional layoffs (35%

total workforce reduction). Stock falls 90%+ from peak. Eric Wu leaves company

entirely in late 2023.

2024

Under CEO Carrie Wheeler, continued turnaround efforts.

Housing market remains challenged with high rates. Progress toward profitability but

still posting losses.

2025

August: Carrie Wheeler steps down as CEO. September: Kaz

Nejatian (ex-Shopify COO) appointed CEO. Keith Rabois becomes Chairman, Eric Wu

rejoins board. Q2 2025: First adjusted EBITDA profitable quarter since 2022 (+$23M).

The Founding Team

Eric Wu (Co-Founder, CEO 2014-2022) - Serial entrepreneur. Previously

founded Movity (acquired by Trulia). Stanford engineering dropout. Stepped down as CEO

in December 2022, left company in late 2023, returned to board in September 2025.

Keith Rabois (Board, Early Investor) - PayPal Mafia member. Khosla

Ventures partner. Instrumental in early strategy and fundraising.

Ian Wong (Co-founder, CTO 2014-2020) - Former

Square data science lead. Built the pricing algorithms that power Opendoor's offers.

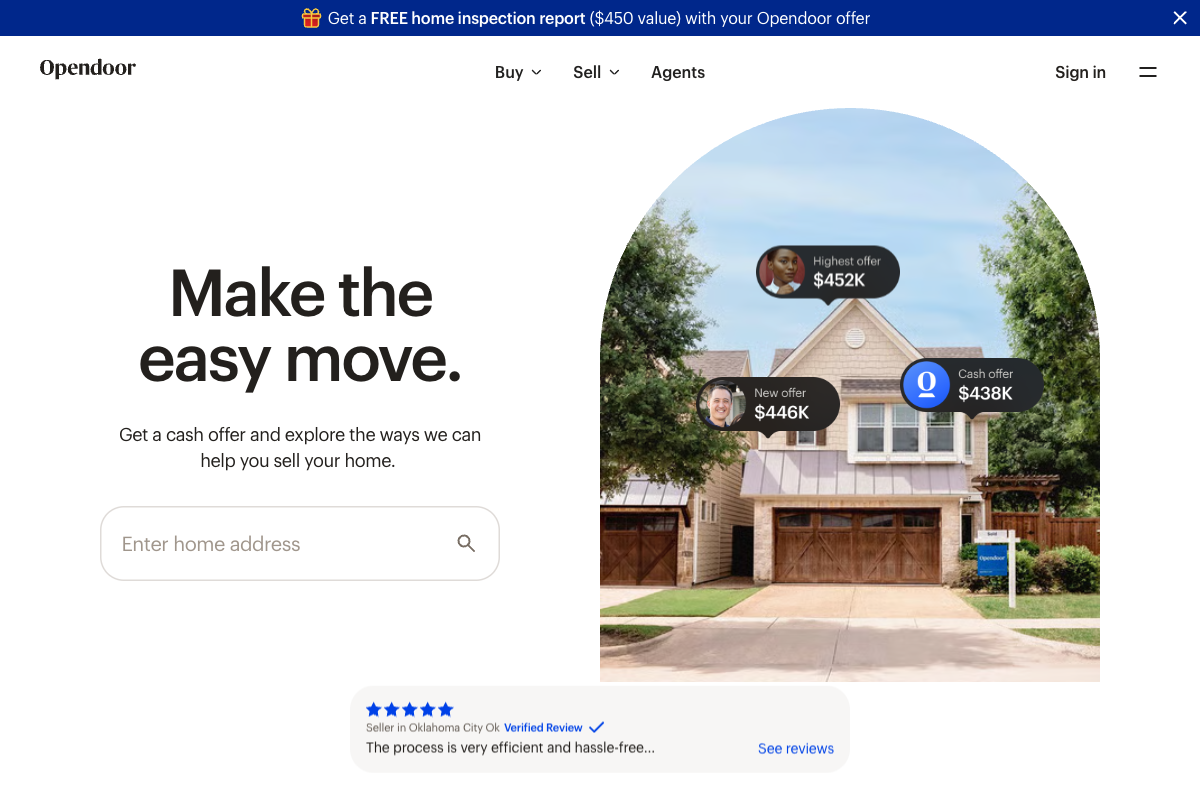

Opendoor's current homepage - "Make the easy move"

Opendoor's core value proposition is simple: sell your home with certainty.

No showings, no repairs, no waiting. It's the "CarMax for homes" model.

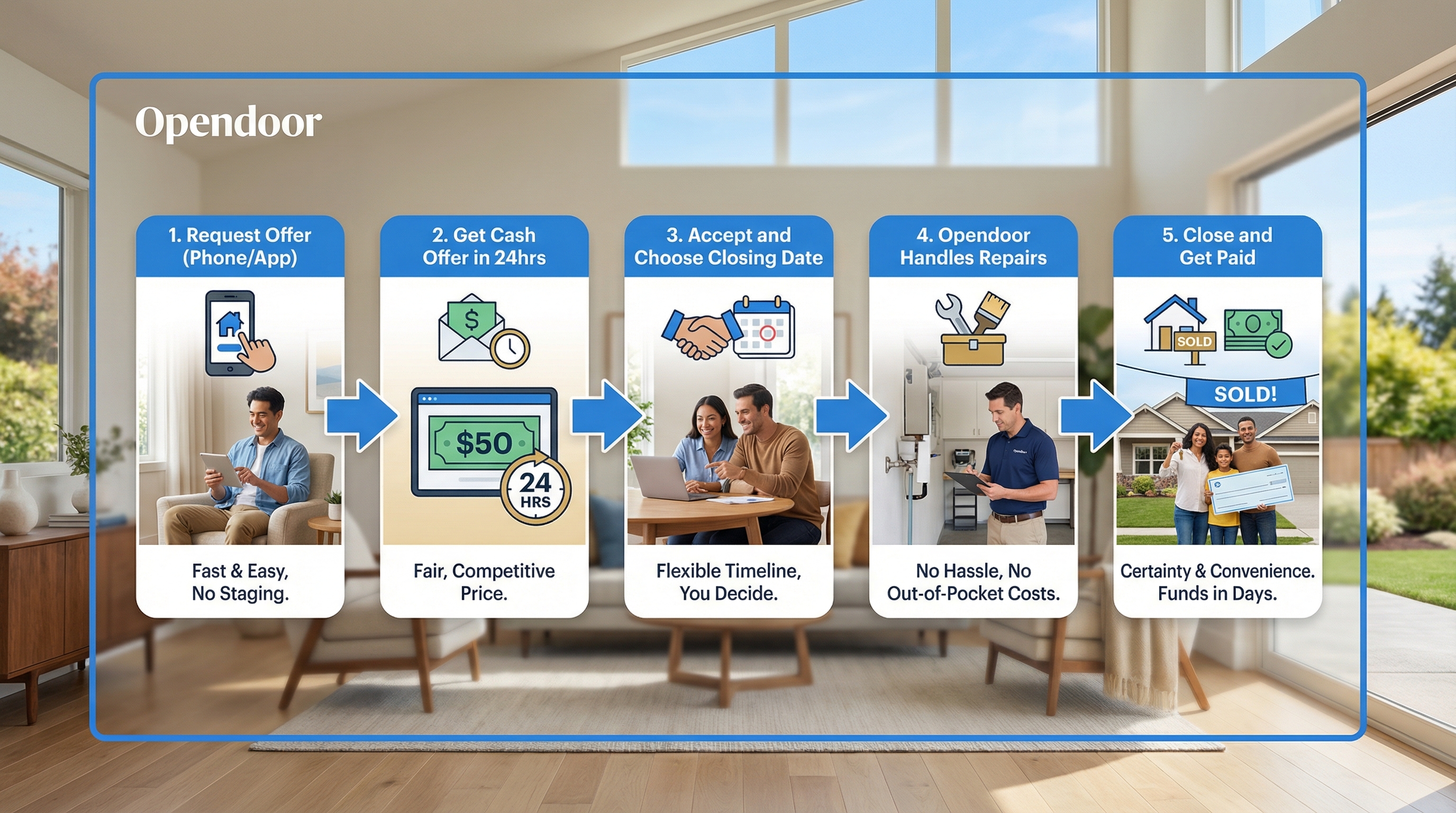

The Selling Journey

Here's how selling to Opendoor works - from request to close in as few as 14 days:

The 5-step selling journey: Request → Offer → Accept →

Repairs → Close

Two Ways to Sell

Sell to Opendoor

Skip the stress of showings and open houses. Pack on

your schedule.

Sell with a preferred agent

List on the market with Opendoor as your backup offer.

Who Uses Opendoor?

Understanding Opendoor starts with understanding who needs this service. It's not

about maximizing sale price - it's about solving real life problems.

The Relocator

Got a job offer in another city. Needs to move in 3 weeks. Can't wait 90 days for a

traditional sale.

Life Transitions

Divorce. Inheritance. Health issues. Sometimes you need out fast, not maximum profit.

The Privacy-Seeker

Doesn't want strangers walking through their home. No open houses. No showing

schedules.

The Busy Professional

Values time over money. Would rather pay 5% than spend 40 hours on showings and

negotiations.

A Seller's Story

Seller Story

Sarah Chen

Phoenix, AZ → Seattle, WA | Job Relocation

Sarah got the call on a Tuesday: her company was promoting her to lead the

Seattle office. Start date: three weeks out.

Her Phoenix home was worth around $420,000. A traditional agent told her it would

take 45-60 days to sell, plus 30 days to close. That's 3 months minimum - she

had 3 weeks.

She could rent it out, but she didn't want to be a long-distance landlord. She

could leave it empty and sell later, but that meant paying two mortgages.

Neither option worked.

Then she found Opendoor. She entered her address at 9pm. By noon the next day,

she had a cash offer for $398,000. Lower than market? Yes. But it solved her

actual problem.

Sarah closed in 14 days, moved to

Seattle, and started her new job on time. She paid ~5% less than market value

but avoided 3 months of stress and carrying costs.

Sarah's Journey with Opendoor

Day 1 - Tuesday Evening

The Panic & The Search

Sarah gets the promotion call. Excitement turns to stress when

she realizes she has to sell her house in 3 weeks. She Googles "sell house fast

Phoenix" at 9pm and finds Opendoor.

Feeling: Anxious, overwhelmed

Day 1 - 9:15pm

Enter Address & Answer Questions

10 minutes filling out basic info about her home - beds,

baths, upgrades, condition. Uploads a few photos from her phone. No commitment yet.

Feeling: Cautiously hopeful

Day 2 - 11:47am

Preliminary Offer: $405,000

Opendoor's algorithm analyzes comparable sales, market trends,

and her home details. She receives an initial cash offer via email and text. It's

real - not a bait number.

Feeling: Surprised, relieved

Day 4

Home Assessment

An Opendoor rep walks through for 30 minutes. They note the

HVAC is original (2008) and the carpet needs replacing. These become repair credits.

Feeling: Nervous about adjustments

Day 5

Final Offer: $398,000

$7,000 deducted for HVAC and carpet. Sarah accepts. She picks

a closing date 14 days out - the day before her flight to Seattle.

Feeling: Decisive, in control

Day 19

Closing Day

Sarah signs digitally. $398,000 minus the 5% service fee

($19,900) and standard closing costs (~$4,000) hits her account. Net: $374,100.

Feeling: Free, ready for Seattle

The math: Sarah netted ~$374K in 19 days. A

traditional sale might have netted ~$395K... in 90+ days. For Sarah, the $21K difference

bought certainty, speed, and peace of mind during a major life transition.

Real Customer Voice

"I chose to go with Opendoor because of the convenience of selling my

home without having open houses, and showings. I have a child on the Autism Spectrum who

has extreme difficulty with change and wouldn't be able to handle people going in and

out of our home. Working with Opendoor was very easy, fast, and professional."

Verified Opendoor Seller, 2025

The Opendoor seller experience starts with a single address

entry

The Traditional Pain Points

95% of sellers find the process stressful. The

biggest pain? Uncertainty - 56% say not knowing if their home will sell in time is the

most stressful part. (Zillow Research)

Time: Conventional process stretches 3-6 months

Showings: Keeping a home "show-ready" while living in it

Staging: $2,000-$7,200 for a 2,000 sq ft home

Uncertainty: Deals fall through, financing fails, timelines slip

Coordination: Aligning sell date with new purchase

The Opendoor Process

1

Enter Address

~10 minutes to complete

2

Get Offer

Within days

3

Assessment

30-min walkthrough

4

Pick Close Date

14-60 days out

5

Get Paid

Cash at close

Selling Options

1. Sell to Opendoor (Cash Offer)

The original iBuyer model. Sell directly to Opendoor for cash. 5% service fee (comparable

to agent commissions).

2. Cash Plus (New 2025)

Get a cash advance upfront, then list on the open market. If it sells for more, you share

the upside.

3. List with Partner Agent

Work with an Opendoor-vetted agent while keeping your cash offer

as backup.

The Tradeoffs

Opendoor typically pays 91-95% of market value. The

tradeoff is speed, certainty, and convenience - not maximum price.

Section 3

How Buying Works

Self-service home buying and Opendoor Exclusives

Opendoor isn't just for sellers. The company has built a buyer experience around

convenience and self-service - particularly powerful after the August 2024

NAR settlement.

The Buying Journey

Here's how buying with Opendoor works - a self-service experience from browsing to move-in:

The 5-step buying journey: Browse → Tour → Offer →

Close → Move In

The magic of discovery: Walking through a sun-filled home

and imagining your future

A Buyer's Story

Buyer Story

Marcus & Elena Rodriguez

Dallas, TX | First-Time Buyers, Dual Income

Marcus works nights as an ER nurse. Elena is a software engineer with

back-to-back Zoom calls from 9am-6pm. Finding time to tour homes together?

Nearly impossible.

Their real estate agent was great, but coordinating schedules meant

maybe one showing per week. At that pace, homes they liked were under

contract before they could see them.

Then Elena found Opendoor Exclusives. Houses they could tour themselves,

at 7pm after her calls or 8am before Marcus slept. No agent coordination. Just

unlock with the app and walk through.

They toured 11 homes in one weekend. On Sunday night, they found it: a 3-bed in

Frisco, listed as an Exclusive at $385,000 - $12K below what similar homes were

fetching on Zillow.

Closed in 21 days with Opendoor's

cash offer backing their financing. No bidding war. No competition. They moved

in 6 weeks after first downloading the app.

The Self-Tour Experience

Saturday 7:30am

Browse & Book

Elena scrolls Opendoor Exclusives over coffee. Finds 4 homes

in their budget within 20 minutes of Marcus's hospital. Books self-tours for when he

wakes up.

Feeling: Excited, in control

Saturday 2pm

Self-Tour #1

They pull up, open the Opendoor app, and tap "Unlock." The

smart lock clicks. They walk through alone, FaceTiming Elena's mom for her opinion.

No agent hovering.

Feeling: This is weird... but awesome

Saturday - Sunday

Tour 11 Homes

Between Marcus's naps and Elena's coding breaks, they tour

every Exclusive in their target area. They'd never have done this with a traditional

agent.

Feeling: Efficient, thorough

Sunday Night

The One

The Frisco house checks every box. Listed at $385K as an

Exclusive. Similar homes on MLS: $397K+. They tap "Reserve" in the app and sign a

contract by 10pm.

Feeling: We found it. This is home.

Day 21

Keys in Hand

Financing clears. Opendoor's appraisal guarantee meant no

last-minute surprises. Marcus and Elena get the keys on a Tuesday morning.

Feeling: Homeowners.

Why Opendoor Exclusives matter: Opendoor owns

~4,500 homes at any given time. Buyers get early access, off-market pricing, and the

freedom to tour on their own schedule. No bidding wars. No contingency races.

Opendoor Exclusives

Opendoor owns significant inventory across 50+ markets. These are "Opendoor Exclusives" -

homes you can tour, buy, and close on without the traditional MLS process.

Opendoor Exclusives: Off-market inventory only available

through Opendoor

Off-Market Access

Homes not on Zillow or Redfin. First-mover advantage.

Self-Touring

Unlock with your phone. Tour on your schedule. No agent

needed.

Skip Bidding Wars

Buy at listed prices directly from Opendoor.

Price Protection

If appraisal comes in low, Opendoor adjusts the price.

Self-Tour Technology

This is particularly relevant post-NAR settlement (August 2024), when new rules required

buyers to sign agreements before touring homes with agents.

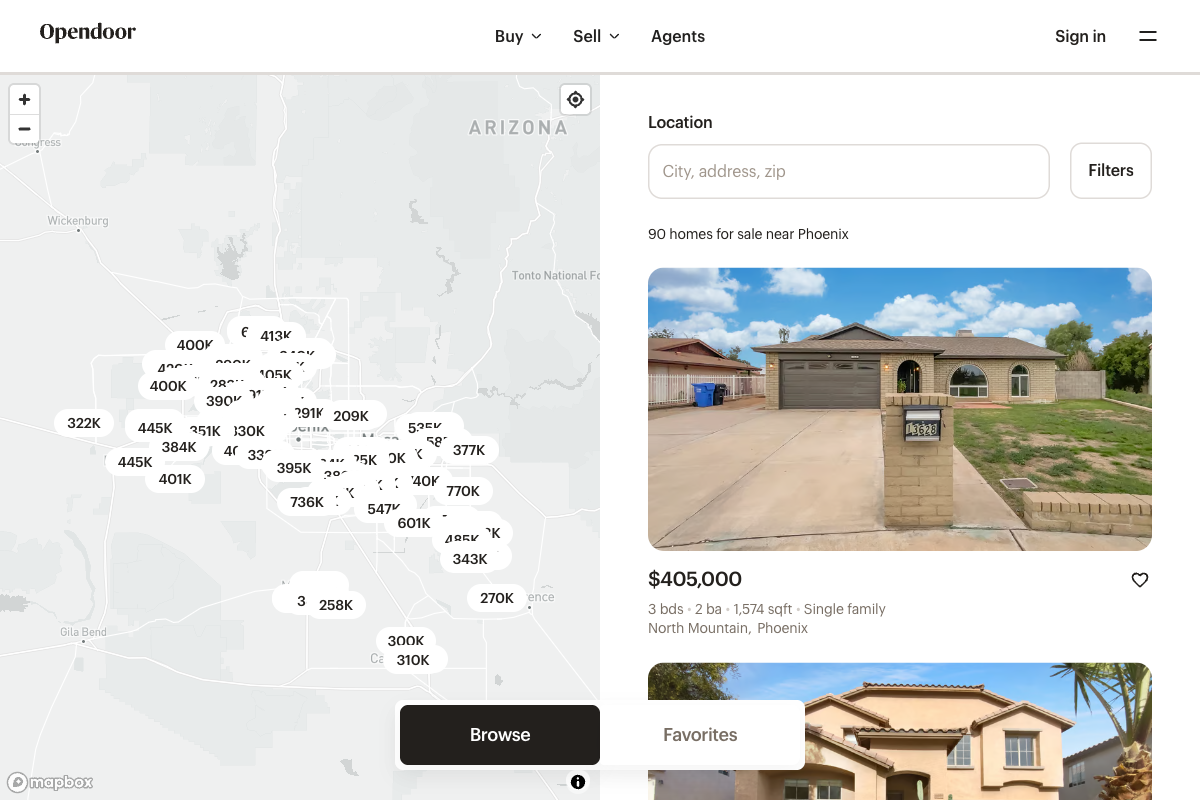

Opendoor homes in Phoenix - one of their largest markets

Try Before You Buy: In select markets (Dallas

pilot), buyers can move in and live in a home before committing to purchase.

Section 4

The Business Model

How Opendoor makes money

The Business Flywheel

Opendoor's business model creates a powerful virtuous cycle - more volume drives better data,

which enables better pricing, which attracts more sellers:

The flywheel: Volume → Data → Pricing → Competitive

Offers → Volume

Core Revenue: Buy-Renovate-Sell

Opendoor's primary business is straightforward: buy homes, make light repairs, and resell on

the open market.

The Unit Economics

Service Fee: ~5% of purchase price (down from 6% historically)

Spread: Difference between buy and sell price (typically 3-7%)

Renovation Profit: Light repairs increase value by more than cost

Target Contribution Margin: 5-7% per home

Q2 2025 Revenue

$1.6B

+36% QoQ

Homes Sold (Q2)

4,299

+5% YoY

Contribution Margin

4.4%

Per Q2 2025

Gross Margin

8.2%

$128M gross profit

Why It's Hard

Capital intensity + low margins + price volatility = high

difficulty. You need billions in inventory, but prices can shift faster

than you can resell.

The Capital Stack

Opendoor uses a mix of equity and debt to finance inventory:

Asset-Backed Credit Facilities: $7.3B in capacity

Non-Recourse: If a home loses value, lenders can't come after

Opendoor's other assets

Spread Business: Borrow at ~7%, sell at ~10% spread = margin capture

Expanding Revenue Streams

Adjacent Services: Title insurance, escrow, mortgage (via partnerships).

These add margin without inventory risk.

List with Opendoor: Earn referral fees when

sellers choose traditional agents instead of cash offers.

Section 5

Market Opportunity

The $2 trillion residential real estate market

The scale of opportunity: Millions of American homes

change hands every year

US Home Sales (2024)

$2T+

~4M transactions

iBuyer Market Share

~1%

Down from 1.3% peak

Opendoor TAM

$1.4T

In serviceable markets

Current Penetration

0.4%

Massive runway

The Structural Opportunity

Real estate has been stubbornly resistant to digital transformation. Why? High prices,

emotional stakes, and entrenched intermediaries.

"Residential real estate is still a $100B/year commission business

where 89% of sellers use a traditional agent. That's not innovation-proof - that's

innovation-ready."

The National Association of Realtors settled a landmark antitrust lawsuit for

$418M. New rules effective August 17, 2024 ended the practice of sellers

automatically paying buyer agent commissions. Buyers must now sign agreements

before touring homes. This disruption opens doors for alternative models like

Opendoor's self-touring and direct buying.

Consumer Expectations — Millennials/Gen Z expect Amazon-like

experiences

Younger buyers grew up with one-click purchases and same-day delivery. They

expect transparency, speed, and digital-first experiences. Traditional 3-6 month

home sales with multiple agents feel antiquated to this demographic, which now

represents the largest share of homebuyers.

Labor Market Fluidity — Remote work = more relocation = more

transactions

Post-COVID remote work policies have untethered workers from office locations.

This has driven migration to lower-cost Sunbelt markets (where Opendoor is

strongest) and increased overall household mobility, generating more real estate

transactions.

Aging Population — Boomers downsizing creates selling demand

Baby Boomers own ~44% of US homes. As they age and downsize, they prioritize

convenience over maximizing sale price - exactly Opendoor's value proposition.

This demographic shift could unlock significant inventory over the next decade.

Mortgage rates rose from ~3% in 2021 to 7%+ in 2024. Higher rates reduce

affordability, decrease transaction volumes, and can pressure home prices.

Opendoor's financing costs also rise with rates, squeezing margins on both ends.

Housing Affordability — Median home price vs income at

historic highs

The median US home price (~$420K) relative to median household income (~$75K) is

at or near all-time highs. This affordability crisis suppresses first-time buyer

demand and overall transaction volumes, limiting Opendoor's addressable market.

Inventory Shortage — "Golden handcuffs" keep owners locked in

~60% of mortgages have rates below 4%. Homeowners are reluctant to sell and give

up these low rates for a new 7% mortgage. This "lock-in effect" has reduced

existing home sales to 30-year lows, constraining the entire market.

Regional Concentration — Sunbelt focus is both advantage and

risk

Opendoor is heavily concentrated in Sunbelt markets (Phoenix, Dallas, Atlanta,

etc.) where housing stock is more homogeneous and predictable. While this aids

their pricing algorithm, it also exposes them to regional downturns - as seen in

2022 when these markets corrected sharply.

Section 6

Competitive Landscape

iBuyers, portals, and the real estate ecosystem

The Real Estate Ecosystem: Key Players

To understand Opendoor's position, you need to understand the complex web of organizations,

regulations, and players that make up the $2 trillion residential real estate market.

NAR (National Association of Realtors)

The powerful trade association with 1.5M+ members that has

shaped real estate for decades. Controls the trademark "Realtor" and historically

enforced the 5-6% commission model through MLS rules.

August 2024

Settlement: NAR agreed to pay $418M and eliminate rules requiring sellers

to pay buyer agent commissions. This is the biggest change to real estate in 50 years -

and creates opportunity for Opendoor.

MLS (Multiple Listing Service)

The database where homes are listed for sale. Historically

controlled by local Realtor associations with restrictive rules. Zillow, Redfin, and

others syndicate MLS data - but Opendoor's Exclusives program bypasses

MLS entirely, listing homes only on Opendoor.com for 14 days first.

Traditional Brokerages

Keller Williams, RE/MAX, Coldwell Banker, Century

21 - The franchise models that dominate residential real estate. Agents are

independent contractors, not employees.

Opendoor isn't trying to replace

agents - they partner with them through the Opendoor Exclusives program and agent

referral network.

Title & Escrow Companies

First American, Fidelity National, Old

Republic - Handle the closing process, title insurance, and escrow.

Opendoor uses these partners but is building more of the closing stack in-house.

Mortgage Lenders

Rocket Mortgage, United Wholesale Mortgage, Wells Fargo

Home Lending - Finance home purchases. Opendoor partners with lenders but

interest rates directly impact their business (higher rates = fewer buyers = longer

holding periods).

Offerpad - Direct iBuyer Rival

Opendoor's most direct competitor. Similar model, smaller scale, more conservative approach.

2024 Revenue: $919M (down 30% YoY)

Strategy: Capital-efficient, regional focus

Differentiator: Free local move, B2B renovation services

Challenges: Stock down 30% in 2025, struggling with scale

Offerpad: Direct iBuyer competitor

Similar process to Opendoor

Zillow - The Cautionary Tale

Zillow launched Zillow Offers in 2018, scaled aggressively, then spectacularly imploded in

November 2021.

"We've determined the unpredictability in forecasting home prices far

exceeds what we anticipated."

Rich Barton, Zillow CEO (November 2021)

What went wrong: "Project Ketchup" used Zestimate

as offer price, algorithm couldn't adapt to market shifts, $500M+ loss in Q3 2021 alone.

2,000 layoffs. Opendoor surviving this period was no small feat.

Zillow: Exited iBuying in 2021

Zestimate: The algorithm that failed

Redfin + Rocket - The New Threat

In 2025, Rocket Companies acquired Redfin for $1.75B, creating a vertically integrated

homebuying stack.

Redfin: Search, agents, listings

Rocket Mortgage: Largest mortgage lender in America

Rocket Homes: Closing services

Redfin: Now "Powered by Rocket"

Compass: Premium brokerage model

Compass - The Off-MLS Play

Compass has 35% of listings as "Private Exclusives" - off-MLS, controversial, potentially

reshaping how homes are marketed.

Leadership Transition: Eric Wu stepped down as CEO

in December 2022. Carrie Wheeler (former CFO) served as CEO from Dec 2022 - Aug 2025. In

September 2025, Kaz Nejatian (former Shopify COO) was appointed CEO, with Keith Rabois

returning as Chairman and Eric Wu rejoining the board. The founders backed the

transition with $40M in PIPE financing, signaling strong conviction in

the turnaround.

KN

Kaz Nejatian

Chief Executive Officer (Sept 2025 - Present)

Former COO at Shopify (2022-2025) where he oversaw merchant

solutions, payments, and capital products. Founded Kash (fintech, acquired 2017).

Queen's University business, University of Toronto law. Known for AI-first approach

and operational excellence. Compensation: $1 base salary, equity tied to stock price

milestones up to $33/share.

LM

Lucas Matheson

President (Dec 2025)

Former CEO of Coinbase Canada, 5 years at Shopify. Overseeing

Corporate Development, FP&A, and blockchain/tokenization initiatives for new

pathways to homeownership.

CS

Christy Schwartz

Chief Financial Officer (Jan 2026)

Promoted from interim CFO after extensive search. Former CFO at

Redfin. Deep proptech finance experience. Leading the path to sustained

profitability.

GL

Giang LeGrice

Head of Operations (Oct 2025 - Present)

Former VP of Operations at Shopify (2019-2025), where she scaled

operations through hyper-growth. 20+ years operations experience across tech,

retail, and e-commerce. Started career as an actuary. University of Manitoba (BCom,

Actuarial Math & Finance). Known as Kaz's "second-in-command" at Shopify - brought

to Opendoor to drive operational excellence and AI-powered efficiency.

CW

Carrie Wheeler

Former CEO (Dec 2022 - Aug 2025)

Served as CFO (2020-2022) before becoming CEO during company's

most challenging period. Led turnaround efforts including cost cutting and path

toward profitability. 25+ years in private equity. Stepped down in August 2025 amid

investor pressure. Currently serves on boards of TKO Group and APi Group.

EW

Eric Wu

Co-Founder, Board Member (Sept 2025 - Present)

Founded Opendoor in 2014. Stanford engineering dropout. Previously

founded Movity (acquired by Trulia). CEO 2014-2022, left company in late 2023.

Returned to board in September 2025 alongside Kaz's appointment. Also co-founder of

NavigateAI. Invested $40M alongside Khosla when Kaz was appointed.

Board of Directors

Keith Rabois - Chairman (Sept 2025). Khosla Ventures partner, PayPal

Mafia member. Original investor and co-founder. Returned as Chairman alongside Kaz's

appointment.

Other notable directors include Cipora Herman

(former Amazon exec) and Jason Kilar (former Hulu CEO, WarnerMedia

CEO).

Section 8

Current State

Latest results and the transition to Opendoor 2.0

Milestone achieved: Q2 2025 was Opendoor's first

adjusted EBITDA positive quarter since 2022 (+$23M). A significant turning point after

years of losses.

Q3 2025: The Transition Quarter

Q3 2025 reflects the deliberate inventory reset under Kaz's leadership - clearing older homes

to build fresh with AI-driven pricing:

Revenue

$915M

Beat estimates by 7%

Homes Sold

2,568

Clearing older inventory

Gross Margin

7.2%

Strong unit economics

Inventory

$1.05B

Leaner, faster turns

Q4 2025 Outlook: Acquisitions expected to increase

35%+ vs Q3 as the new AI-driven approach takes hold. Targeting breakeven Adjusted Net

Income by end of 2026.

Trump Housing Policy (Jan 2026): When Trump

announced plans to ban institutional home-buying, Opendoor stock initially dropped 10%.

CEO Kaz Nejatian clarified on X: "We're not institutional investors, our job is to help

people buy homes. We don't hold the homes!" Stock recovered after the clarification.

Recent Developments

CEO Transition (Sept 2025): Carrie Wheeler stepped down in August. Kaz

Nejatian (ex-Shopify COO) appointed CEO. Keith Rabois returns as Chairman, Eric Wu

rejoins board.

$40M Investment: Khosla Ventures and Eric Wu invested $40M alongside

new CEO appointment.

Stock Surge: Stock jumped 78% on CEO announcement news.

Opendoor 2.0: New AI-first strategy focused on software and operational

excellence.

The Turnaround Narrative

After near-death experience in 2022-2023 (90%+ stock decline, multiple layoffs), Opendoor has

stabilized. The question now: is this a launching pad for renewed growth, or a lower

plateau?

Section 9

Risks & Challenges

What could go wrong

Weathering challenges: Understanding the risks ahead

Macro Risks

Interest Rate Sensitivity

Higher rates = fewer buyers = longer holding periods = margin compression. Opendoor's

financing costs also rise with rates.

Housing Price Volatility

The core risk. A 5-10% national price decline could wipe out years of margin. The

2022-2023 experience showed this isn't theoretical.

Transaction Volume

Existing home sales remain near 30-year lows. "Golden handcuffs"

- homeowners locked into low-rate mortgages - constrain inventory.

Business Risks

Capital Intensity

iBuying requires billions in inventory. Capital costs are high, and access can tighten

quickly in downturns.

Pricing Algorithm Risk

The algorithm must be more accurate than the market. Systematic mispricing (like Zillow)

can compound quickly.

Competition

Rocket/Redfin combination. Compass off-MLS strategy. Traditional

agents still control 89%+ of transactions.

Operational Risks

Geographic Concentration: Heavy Sunbelt exposure is both opportunity

and risk

Execution Risk: New CEO, new strategy, organizational change

Regulatory: Real estate is heavily regulated; rules can change

Brand/Trust: iBuyer reputation still being established with consumers

The bear case: iBuying is structurally challenged.

Margins too thin, capital too expensive, price risk too high. Opendoor survives but

never achieves venture-scale returns.

Section 10

Opendoor 2.0

A refounding under new leadership

The vision: Buying a home as seamless as buying a car

from Tesla

The New CEO: Kaz Nejatian

In September 2025, Opendoor brought in Kaz Nejatian, former COO of Shopify,

to lead a complete transformation. His compensation? $1 annual salary -

everything else is tied to stock performance. Total skin in the game.

"We are refounding Opendoor as a software and AI company. In my first

month as CEO, we've made a decisive break from the past."

Kaz Nejatian, CEO

The Transformation

Under Kaz's leadership, Opendoor is being completely rebuilt - from an iBuyer with technology

to a technology company that buys homes:

The refounding: From hedge fund mentality to AI-native

platform

The Philosophy Shift

From hedge fund to tech company: "Our job is not to run a hedge fund

that aims to make money off of macroeconomics. Our job is to buy and sell lots and lots

of homes at very tight spreads and make money off of transaction volume."

The mission: "If we can make buying, selling, and owning a home easier

and less terrible, the world will be a better place. If we do that, we'll make money

along the way."

The urgency: "The fact that the average age of a

person who buys their first home now is 40 is deeply depressing. That has such negative

implications for our society."

The "Default to AI" Mandate

Within his first weeks, Kaz sent a company-wide memo requiring employees to "default to AI"

in their work. The specific mandates:

Kaz's Day-One Changes

Return to office: Mandatory in-person work to increase velocity

No more consultants: "Decisions that executives should be making"

were being outsourced

AI-first operations: Staff were manually copying PDF data into

spreadsheets - that stops

Founder mode: "We are ditching manager mode. We're firmly in

founder mode now."

Weekly accountability: Progress tracked at accountable.opendoor.com

The Elon Musk Playbook: Kaz is running the classic

"new CEO turnaround" - $1 salary (up to $2.8B in equity tied to stock milestones),

relentless X updates on progress, cutting consultants, and demanding founder-level

intensity from the entire organization.

Immediate Results

Acquisition Speed

2.3x

120 → 282 homes/week by Nov 2025

New Products Launched

12+

AI-powered features in first month

"Opendoor's procurement team is so AI-pilled that they are now using

AI tools to cancel useless SaaS contracts across the board. In one area, we will soon go

from paying 10 (ten!) different providers to paying just one + our internal AI tool,

saving us million $+ a year."

Kaz Nejatian, on X (December 2025)

"First pic took 10 years of work without AI. Second pic took

10 weeks of work with AI."

Kaz Nejatian, on X (January 2026) — on Opendoor's expansion

The Vision: Everything a Homeowner Needs

"Buying a home will in the future be as seamless as buying a car from

Tesla. Right now, homeowners have to deal with a bunch of different companies, brokers,

agents. We're going to fix this - and over time, we'll add everything a homeowner needs

when they need it, all bundled into one simple experience."

Kaz Nejatian

The AI-Native Platform

Kaz's vision is to build a single platform that handles everything a homeowner needs -

powered by AI at every step:

One platform, every service: The Opendoor ecosystem

New Product Initiatives

Opendoor Checkout

"The buy now button for homes on the internet" - tour and

submit offers directly, no agent needed

Try Before You Buy

Move in, live in the home, return it if you don't love it

(launched in Dallas)

AI Automation

Eliminating manual work - no more copying PDFs into

spreadsheets

Asset Tokenization

"I can't imagine a future where real estate is not tokenized"

- exploring blockchain pathways to ownership

Path to Profitability

The goal: "By the end of next year, we will drive

Opendoor to breakeven Adjusted Net Income on a 12-month go-forward basis." The path:

more sellers, better pricing, faster resales, ruthless efficiency.

What to Watch

Contribution Margin

Can they sustain 5%+ consistently?

Acquisition Velocity

Maintaining the doubled pace?

Product Adoption

Checkout, Try-Before-Buy traction

Cash Flow

Operating cash flow positive?

The Bottom Line

Opendoor has survived what Zillow couldn't. Under Kaz's leadership, the company is being

refounded - not as a real estate speculation play, but as a technology company that happens

to operate in real estate. The question isn't whether the vision is right. It's whether they

can execute fast enough.

The bet: If Opendoor can capture even 3-5% of the

$2T residential market with sustainable margins, it becomes a $50B+ company. Kaz

believes it can become a "multi-hundred billion dollar company." That's the opportunity.

Section 11

Financial Overview

Key metrics and financial health indicators

Financial Summary

The situation: Opendoor lost $2.7 billion from 2021-2024 and stock fell 98.7%. New CEO Kaz Nejatian took over September 2025. Stock has recovered +294% since the April low.

The financials: $962M cash on hand, 15+ quarters of runway, contribution margin at 2.2% (down from 4.7% in Q1). Targeting breakeven by end of 2026.

What to watch: Q4 2025 earnings on February 26, 2026. Contribution margin on new inventory is the key indicator.

Q3 2025 Financial Snapshot

The most recent quarter reflects Kaz's "clearing the decks" strategy — selling old inventory at compressed margins while ramping up AI-driven acquisitions.

Revenue

$915M

Beat guidance by 5%

Adj. EBITDA

$(33)M

Below guidance range

Net Income

$(90)M

vs $(78)M Q3 2024

Contribution Margin

2.2%

Down from 4.7% Q1

Homes Sold

2,568

Clearing old inventory

Homes Purchased

1,169

AI-priced acquisitions

Kaz's View: "We are refounding Opendoor as a software and AI company. Our business will succeed by building technology that makes selling, buying, and owning a home easier — not from charging high spreads and hoping the macro saves us."

The 10 Metrics That Matter

These are the numbers Kaz and investors are watching most closely. Each tells a different part of the turnaround story.

1. Revenue (Quarterly)

$915MQ3 2025

Revenue beat guidance ($875M high-end) by 5%, but declined 33% year-over-year as Opendoor deliberately reduced inventory.

Why Kaz cares: Revenue will drop ~35% in Q4 as old inventory clears. The bet is that AI-priced homes acquired now will generate healthier revenue in 2026.

2. Adjusted EBITDA

$(33)MQ3 2025

Missed guidance of $(21-28)M loss. EBITDA excludes interest, taxes, depreciation, and one-time charges — showing core operational profitability.

Why Kaz cares: Q4 guidance is $(45-55)M loss as margins compress further. Kaz is targeting Adjusted Net Income breakeven by end of 2026.

3. Contribution Margin

2.2%Q3 2025

The profit margin on each home after direct costs (acquisition, repairs, holding, selling). Dropped from 4.7% in Q1 as old inventory sold at losses.

Why Kaz cares: This is THE metric. Kaz says the old Opendoor relied on "wide spreads" (high margins). The new strategy: high velocity with tighter but consistent margins. If new AI-priced inventory achieves 4%+, the model works.

4. Net Income (Loss)

$(90)MQ3 2025

GAAP net loss increased from $(78)M in Q3 2024. This includes all expenses — the true bottom line showing Opendoor is still burning cash.

Why Kaz cares: Accumulated losses since 2021 total ~$2.7B. Kaz's credibility depends on bending this curve toward zero by late 2026.

5. Cash & Liquidity

$962M

Unrestricted Cash

$490M

Restricted Cash

$1.45B

Total Cash

Strong balance sheet with more cash than long-term debt ($439M). Restricted cash is tied to inventory financing and can't be used freely.

Why Kaz cares: At ~$60M quarterly burn, Opendoor has 15+ quarters of runway. This gives Kaz time to execute without dilutive capital raises.

6. Homes Sold (TTM)

~11,000Trailing 12 months

Q3 2025 saw 2,568 homes sold (down 29% YoY). Volume is intentionally low as Opendoor clears legacy inventory and rebuilds with AI-priced homes.

Why Kaz cares: Volume drives revenue and data. Kaz's stated goal: 6,000 homes/quarter by Q4 2026 — a 5x increase from current levels.

7. Inventory Aging (>120 days)

ElevatedLegacy inventory

Homes older than 120 days incur significant holding costs and typically sell at losses. Q2 showed a high portion of aged inventory — a key reason Q3 margins dropped.

Why Kaz cares: "Clearing the decks" means selling this old inventory at compressed margins. Once cleared, new AI-priced inventory should have lower aging and better margins.

8. AI Products Deployed

12+Products launched

In Kaz's first month, Opendoor launched 12+ AI products: automated home assessments (10 min vs 1 day), repair scoping, title/escrow automation, and pricing models.

Why Kaz cares: "We are refounding Opendoor as a software and AI company." AI reduced assessment time 95% and nearly doubled acquisition velocity (120→230 homes/week in 7 weeks).

9. Operating Cash Flow

$979MYTD 2025

Strong operating cash flow YTD, largely because inventory declined by ~$1.1B. Cash generated from selling homes faster than buying them.

Why Kaz cares: This isn't "real" operating improvement — it's from shrinking the business. True operational cash flow improvement will come from profitable unit economics on new inventory.

10. Market Cap & Stock Volatility

$6.4B

Market Cap

3.69

Beta (volatility)

$0.51-$10.87

52-Week Range

Stock is up +341% over 12 months but extremely volatile (beta 3.69 = 3.7x market movements). 52-week range shows a 21x swing from low to high.

Why Kaz cares: Kaz took $0 salary and ~$1B in equity compensation. His wealth is directly tied to stock performance. Every earnings call is high-stakes.

Understanding Contribution Margin

Contribution margin measures profit per home after direct costs. It's the most important metric for evaluating Opendoor's unit economics.

How it works: Buy a home for $300K → Fix it for $15K → Pay $5K in holding costs → Pay $8K in selling costs → Sell for $340K. Result: ($340K - $300K - $15K - $5K - $8K) / $340K = 3.5% margin

At 2.2%, Opendoor keeps $2.20 for every $100 in revenue. That's tight margins with little room for error.

Contribution Margin Trend

Quarter

Margin

Notes

Q1 2025

4.7%

Healthy margin

Q2 2025

4.4%

Slight decline

Q3 2025

2.2%

Clearing old inventory

Q4 2025

TBD

Results: Feb 26, 2026

Why Q3 margin dropped: Opendoor deliberately cleared older, overpriced inventory from the previous management era. Management expects margins to recover as newly-priced homes flow through.

Balance Sheet Strength

Despite ongoing losses, Opendoor has a strong balance sheet with more cash than debt.

Unrestricted Cash

$962M

Total Cash (incl. restricted)

$1.45B

Long-term Debt

$439M

Negative net debt: Opendoor has more cash ($962M) than long-term debt ($439M). At $61M quarterly losses, they have 15+ quarters (~4 years) of runway before needing additional capital.

Stock Price History

Date

Price

Context

Feb 2021

$39.24

All-time high (SPAC peak)

Nov 2021

$24.00

Zillow exits iBuying

Dec 2022

$3.00

Rate shock, $1.4B annual loss

Apr 2025

$0.51

All-time low (delisting threat)

Sep 2025

$9.26

Kaz equity raise

Jan 2026

$6.70

Current (+294% from April low)

Scenario Analysis

Bull Case

25% probability

$15-25

Margin recovers to 4%+, velocity 4x, AI creates competitive moat

Wall Street is divided on Opendoor. Here's what different sources report as of January 2026.

Analyst Consensus

SELL / HOLD

1 Buy · 5 Hold · 3 Sell

Avg Price Target

$1.60 - $3.56

Range: $0.91 to $8.40

AI Analysis (Danelfin)

7/10 BUY

57% chance to outperform

Price target disconnect: Current stock price (~$6.70) is ABOVE most analyst targets. Many analysts see 54-76% downside, while the stock has already rallied 1,000%+ from lows. Analysts may be slow to update targets, or the stock may be overvalued.

Bull vs Bear Case

The Bull Case

AI transformation could genuinely fix unit economics

If 5-7% contribution margin achieved, stock re-rates higher

New leadership making hard decisions (clearing bad inventory)

The metric to watch: Contribution margin on newly-acquired inventory. If it recovers to 4%+ on homes purchased under Kaz's pricing models, the turnaround thesis is validated. If it stays below 2.5%, the path to profitability becomes much harder.